The lecture was held in the winter term 2001/2002 at Humboldt-University, Tue 14.15 Dorotheenstr. 24, room 111.

The aim was to describe the mathematical and computational aspects of risk management for the trading book of banks.

This was the reading list.

The slides were available in two versions (last updated 2002-10-17):

Topics

- 1. The Need for Risk Management (30.10.2001)

- 2. Overview and Taxonomy (06.11.2001)

- 3. VaR and TCE (06.11.-13.11.2001)

- 4. Delta-Gamma-Normal Models: General Properties (13.11.-20.11.2001)

- 5. Delta-Gamma-Normal Models: Fourier-Inversion (20.11.-11.12.2001)

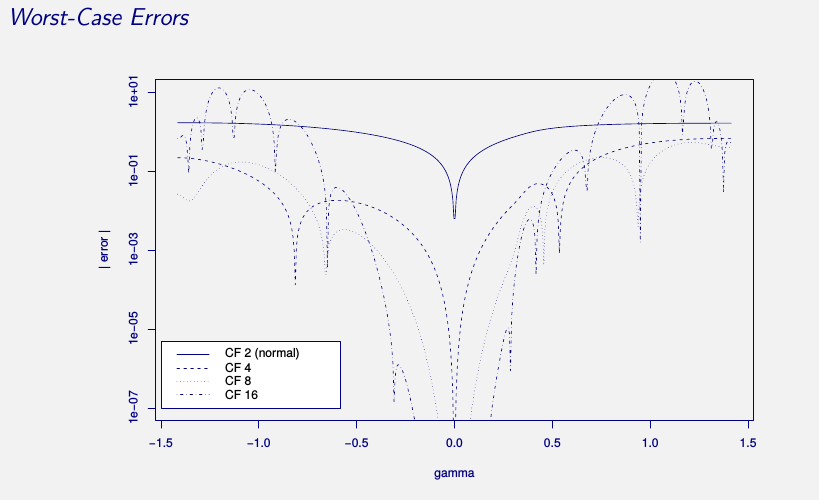

- 6. Delta-Gamma-Normal Models: Cornish-Fisher Approximation (11.12.2001-08.01.2002)

- 7. Delta-Gamma-Normal Models: Saddle-Point Approximations (22.01.2002)

- 8. Delta-Gamma-Normal Models: Other Approximations (22.01.2002)

- B. Monte-Carlo Simulation (29.01-12.02.2002)